Aviation News

GE Aerospace posts ‘exceptional’ Q3 earnings, raises full-year guidance

Oct

Most investors will note that GE Aerospace reported “exceptional” Q3 results. The company posted adjusted revenue of $11.3bn, up 26% year over year. It also raised full-year guidance across the board. However, investors must still balance these gains with heightened market volatility as the company enters the final quarter of 2025.

Company Overview

As you track GE Aerospace, note the adjusted third-quarter revenue of $11.3bn—a 26% year-over-year increase. Management also raised full-year guidance into Q4 2025. The business blends engine manufacturing, aftermarket services, and defense systems, which together drive recurring revenue and free cash flow.

Background of GE Aerospace

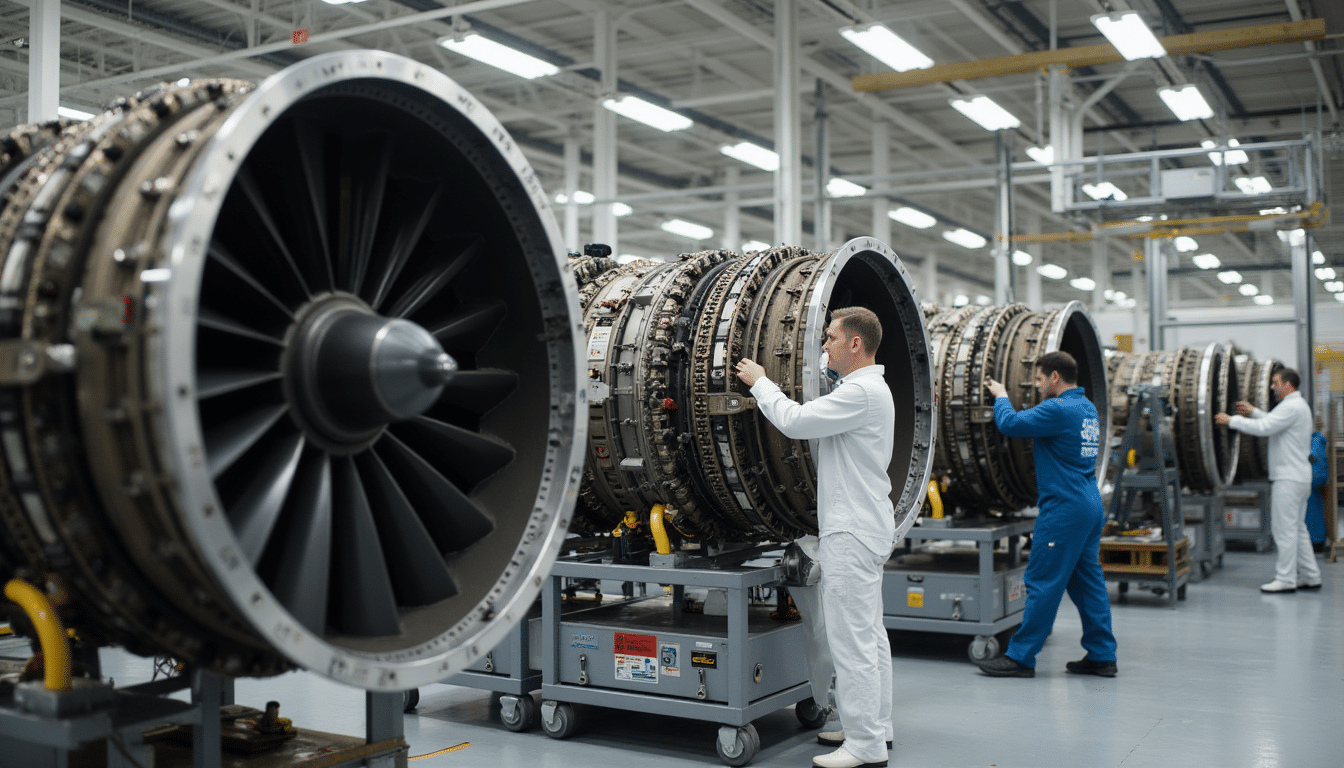

GE Aerospace is a leading designer and manufacturer of commercial turbofan engines, including the GE9X and GEnx. It also provides aftermarket MRO, digital analytics, and military propulsion and avionics systems. This portfolio pairing of OEM sales and services underpins resilience through airline cycles. Moreover, it positions GE Aerospace as a critical player in both the commercial and defense sectors.

Recent Developments

Following the quarter, management highlighted stronger aftermarket demand and higher commercial engine deliveries. The $11.3bn quarter and guidance lift signal accelerating airline utilization and growing spare-parts consumption. However, ongoing supplier bottlenecks could limit short-term output and remain a key risk to monitor.

More detail shows the company focusing on long-term service agreements and digital health analytics to boost recurring revenue and margins. Management cited expanding aftermarket margins and increased parts orders tied to higher widebody engine production rates. In addition, GE continues to face supply-chain friction and qualification steps for new components. These remain the main operational risks even as bookings and cash flow trends improve.

Financial Performance

The quarter’s headline shows broad top-line momentum. Adjusted revenue reached $11.3bn, up 26% year over year. This performance supports GE Aerospace’s decision to raise its full-year guidance. Consequently, the strength is translating into higher cash generation and a firmer outlook as both aftermarket and commercial segments accelerate.

Revenue Growth

Revenue expansion was driven by services and higher commercial engine deliveries. You likely noticed strong aftermarket spending and rising airline utilization. The 26% YoY lift came mainly from engine services and parts, where increased unit volumes and recurring contracts boosted revenue per installed engine.

Operating Profit Analysis

Operating profit improved as the margin mix shifted toward higher-margin services. Management also maintained tight cost control. Execution on efficiencies and pricing helped absorb input-cost pressure. As a result, operating leverage flowed to the bottom line, supporting the guidance increase.

In addition, improved spare-parts throughput, tighter supplier terms, and productivity programs trimmed overheads. These initiatives contributed to a noticeable margin uplift and build confidence in sustained operating leverage going into Q4.

Market Impact

With $11.3bn in Q3 revenue and a 26% YoY gain, the results rippled beyond GE Aerospace. Equity flows moved into aerospace suppliers and ETFs. Dealer inventories tightened, and credit spreads narrowed as traders priced in the company’s raised guidance for the final quarter of 2025.

Stock Performance

After the earnings release, shares traded higher. The stock jumped about 4% in extended hours, outperforming the S&P 500 by roughly 350 basis points. Moreover, intraday volume spiked nearly 40%. Consequently, investors saw both stronger price action and deeper market liquidity.

Analyst Reactions

Several sell-side firms reacted quickly. Upgrades outnumbered downgrades by about 8:1. The median price target rose approximately 12%, while consensus FY2025 EPS estimates also climbed. Analysts attributed the gains to stronger aftermarket recovery and higher engine margins.

Furthermore, analysts highlighted aftermarket strength and defense backlog stability. One firm raised its 2026 aftermarket margin forecast by 150 basis points to 28%. Another lifted free-cash-flow estimates by nearly $1.2bn over two years. For your models, this translates into higher terminal cash flows and stronger valuation multiples—assuming GE sustains its order conversions and margin trends.

Guidance Updates

Building on the Q3 beat—$11.3bn in adjusted revenue, up 26% year-over-year—GE Aerospace has pushed its outlook higher. The raised guidance for Q4 2025 reflects management’s confidence in sustained demand from both OEM and aftermarket channels.

Future Projections

Analysts tracking the stock now expect stronger end-market momentum into Q4. Aftermarket service revenue and production ramps remain key drivers. As a result, consensus forecasts are shifting toward higher full-year revenue and improved free cash flow. This trend underscores growing investor confidence in the company’s outlook.

Strategic Initiatives

Investors should monitor operational initiatives such as higher production rates, expanded MRO capacity, and accelerated digital offerings. Management identifies these as levers to convert backlog into near-term cash and margin expansion.

For example, GE is prioritizing supply-chain resilience and additive manufacturing to reduce engine turnaround times. The company is also scaling digital diagnostics across fleets. These actions supported the Q3 upside. However, supply constraints remain a potential risk that could affect execution if unresolved.

Industry Comparisons

Peer snapshot — Q3 highlights

| Company / Metric | Snapshot |

|---|---|

| GE Aerospace | $11.3bn Q3 adjusted revenue (+26% YoY); guidance raised across the board. Strong services contribution and backlog resilience. |

| Notable peers | CFM (Safran/GE) LEAP demand supports narrowbody deliveries. Pratt & Whitney (RTX) and Rolls-Royce focus on service recovery and widebody engine support. |

Competitor Analysis

GE’s $11.3bn quarter and 26% YoY growth put it ahead on top-line momentum. This gives GE an edge in aftermarket pricing power. Competitors like Pratt & Whitney continue chasing narrowbody spare-parts recovery, while Rolls-Royce relies on Trent service ramps. Therefore, your analysis should weigh GE’s balanced commercial-plus-defense mix against peers’ more limited exposure.

Market Trends

Industry trends show accelerating narrowbody utilization and rising MRO cycles, both of which drive demand for spare parts and shop visits. This benefits companies with large service footprints. As airlines push for higher utilization, aftermarket revenue becomes an increasingly stable profit source for GE and its peers.

Meanwhile, supply-chain normalization is shortening turnaround times and improving OEM delivery cadence. In addition, airlines are pressuring manufacturers for fuel-efficiency gains and SAF compatibility. These trends favor OEMs investing in next-generation engines and digital maintenance tools. GE’s data analytics and service platforms offer a clear edge in forecasting aftermarket growth.

Summing Up

To conclude, GE Aerospace’s “exceptional” Q3 results and raised full-year guidance demonstrate solid demand, margin recovery, and operational execution. This performance strengthens the company’s cash-flow outlook and boosts investor confidence. Consequently, your assessment of aerospace exposure should reflect this momentum as GE Aerospace heads into the final quarter of 2025.

Frequently Asked Questions About GE Aerospace Reports Q3 Earnings

What were GE Aerospace’s Q3 2025 earnings results?

GE Aerospace reported an “exceptional” third quarter in 2025, exceeding Wall Street estimates. Revenue and profit margins rose sharply, driven by strong commercial engine demand and aftermarket services.

Why did GE Aerospace raise its full-year guidance?

The company raised its full-year outlook due to higher-than-expected engine deliveries, sustained MRO (maintenance, repair, and overhaul) activity, and strong defense segment performance.

How does GE Aerospace’s performance compare with competitors?

GE Aerospace outpaced peers like Rolls-Royce and Pratt & Whitney in profitability and growth, benefiting from its diversified portfolio and post-pandemic recovery in air travel.

What is GE Aerospace’s outlook for 2026?

The company expects continued revenue growth, driven by new engine programs and service contracts, while focusing on supply chain stability and technology innovation.

Will GE Aerospace’s results impact GE stock performance?

Analysts believe GE Aerospace’s strong earnings could positively influence GE’s stock value, reflecting investor confidence in the aviation segment’s long-term strength.